- BlueRock Agency

- Retirement Solutions

Retirement Solutions

Retirement Income Growth & Protection

BlueRock Group is a leading national independent insurance and financial services firm with agents throughout the USA to serve our clients. We specialize in retirement income protection and growth solutions. As an independent firm, we are licensed and contracted with many major insurance carriers that allow us to provide the right solution to meet clients’ needs. These solutions include but are not limited to 403b, 457, indexed annuities, and IUL’s for teachers and public employees. Our #1 objective is to protect what you have worked hard to accumulate in life with zero market risk.

Our licensed professionals are licensed in multiple states and contracted with several carriers to represent the best retirement solutions for teachers, public employees, and the private sector. With our carrier partners, we are an approved vendor in most school districts, universities, and municipalities throughout the nation.

We specialize in retirement income solutions and with our major insurance and financial company partners we are not limited to one company or product. Retirement is not a one size fits all. In working with us you will never be charged a penny for our services. Unlike some financial services firms that charge a fee for their services based on assets under management.

When you work with one of our retirement specialists you have a team of experts working on your case. After we have conducted your retirement needs analysis we put together a custom solution for you based on your current retirement savings, retirement goals, and when you would like to retire.

As a client of ours, we will educate you along the way so you can make an informed and intelligent decision about your retirement. After all, this is your retirement we are talking about.

Recent news headlines and what it can mean for your retirement

Is Stock Market Crash 2.0 Imminent? This has been a “buckle up and hold on” type of year for investors. The unprecedented coronavirus disease 2019 (COVID-19) pandemic created a level of panic and uncertainty that Wall Street had never contended with before. Ultimately, the broad-based S&P 500 lost a whopping 34% of its value in just 33 calendar days. For context, it’s historically taken the S&P 500 an average of 11 months to shed 30% of its value during bear markets.

According to the Retirement Risk Readiness Study from Allianz Life, nearly half of Americans (49%) believe a stock market crash is the biggest threat to their retirement income. It’s a fair concern. For most of us, a 30% drop in the portfolio balance wipes out years of savings. That can be devastating, particularly if you’re behind schedule already, you’d planned to retire within the next few years, or you’re already retired. If any of that sounds like you, it’s time to play some defense with your finances — so a future crash won’t ruin your retirement.

People often treat their retirement savings plans as if inflation isn’t a factor, but it certainly is. Over the past three decades, annual inflation has been about 3%, on average. It’s incredible that we don’t give inflation its due attention for all the hand wringing we do to stretch our money further in other ways. Inflation gradually pushes up the prices of goods and services, and your money won’t go as far if you ignore it. If inflation occurs at the average rate in 2019 and 2020, it will cost you 6% more to purchase the same goods and services in 2021 than it does right now.

Inflation erodes the value of investments and savings.

If you’re among the many folks socking away money in investments and savings for retirement, you need to be aware that inflation will effectively diminish their value over time. If you’ve saved $5,000 per year for 30 years, for example, you’ll have a nice $505,365 at the end of the period, assuming an average 7% return each year, an average for the stock market. Sounds impressive, doesn’t it? And it is.But it’s also not as much as it seems at first blush, because of inflation. The future value of the $505,365 will be roughly the value of $208,204 now. You’ll be sitting on the same pile of dollars, but they’ll purchase less than they do now, because of inflation. Put another way, the costs of goods and services will be steadily advancing because of inflation, so you’ll need to meet the price tags of the future.

Understanding Your Retirement

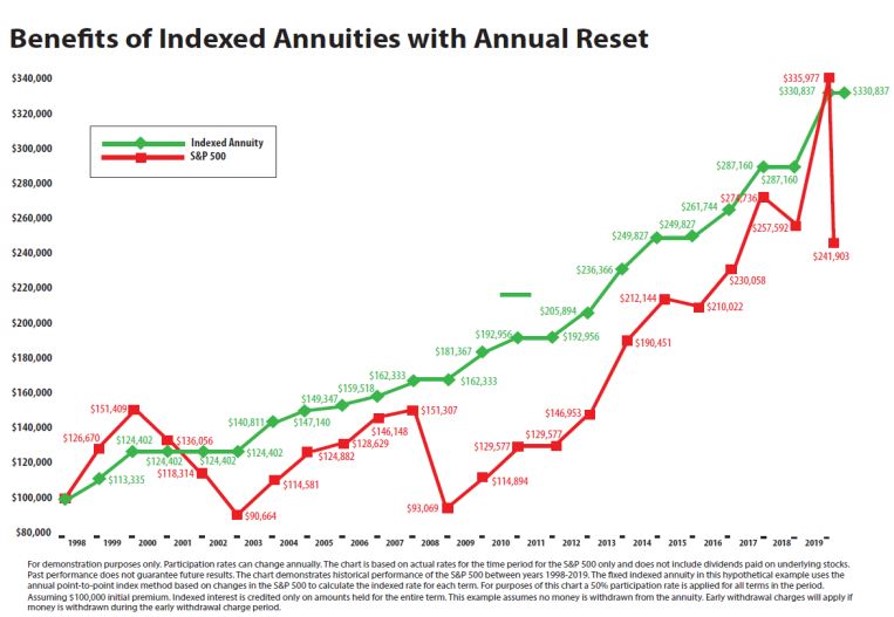

The core of our retirement plans are based on minimizing market risk. When your money is in the stock market you are exposed and have major financial risk and the market can turn on a dime right when you are ready to retire and lose years worth of retirement savings.

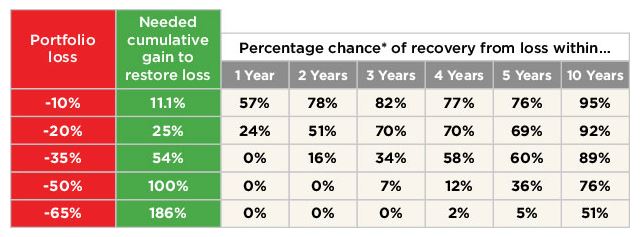

We educate our clients on the power of market gains and losses. Take a look at this chart below. If you lose just -10% in your portfolio you need 11.1% cumulative gain just to get back to even before the loss occurred.

Extremely powerful! The solutions we focus on with our clients have 0 market risk. If the market dives your gains are locked in and can not go backwards.

Steady consistent growth is the key to a successful retirement.

Types of Retirement Solutions

403b – A 403(b) plan is a retirement plan for certain employees of public schools, tax-exempt organizations, and ministries. Individual 403(b) accounts are established and maintained by eligible employees. The employer may determine the financial institution(s) at which individual employees may maintain their 403(b) accounts.

457b – 457(b) Deferred Compensation Plan is an employer-sponsored plan that allows employees to deduct pre-tax dollars from their paychecks and contribute the monies into a retirement savings plan. The 457(b) plans pre-tax status is similar to the traditionally offered 403(b) retirement savings plan. 457(b) plans are eligible governmental supplemental retirement plans and as such, are not subject to qualified plan distribution rules. Plans of deferred compensation described in IRC section 457 are available for certain state and local governments and non-governmental entities tax-exempt under IRC 501. They can be either eligible plans under IRC 457(b) or ineligible plans under IRC 457(f). Plans eligible under 457(b) allow employees of sponsoring organizations to defer income taxation on retirement savings into future years. Ineligible plans may trigger different tax treatment under IRC 457(f).

Tax-Free Retirement Account / Indexed Universal Life – Upside Potential. Downside Protection. One of our most popular and flexible plans! In addition to death benefit protection, an Indexed Universal Life Insurance product offer cash value accumulation potential. This means policy values can be placed into one or multiple Indexed Crediting Strategies plus a fixed account to diversify your growth strategy. The indexed strategies offer upside accumulation value potential in your life insurance policy based in part on the performance of a major index. All of the indexed strategies we recommended offer downside protection from loss with a 0% Floor Guarantee. In addition, the IUL plan offers Living Benefits. Living Benefits are a life protection solution to protect you when life happens. Terminal illness, Chronic Illness, Critical Illness, Cancer, Heart Attack, Stroke, etc.

Retirement Resources

Retirement planning takes research and time. Our retirement income specialist will educate you and create a custom plan just for you.

Reasons People Don’t Have Enough or Lose Retirement Savings

Start too late to begin saving for retirement. When you are young you have many more retirement solution options available and Time. Time is always on your side when it comes to retirement. It’s never too early or too late to start saving.

Stock Market loss. Many advisors recommend that you diversify your portfolio to balance the risk. Even if you are diversified in the stock market you still have market risk even with mutual funds. The stock market is volatile and has wiped many investors as they are about to retire causing them to delay retirement or live below their comfort level.

Inflation. One of the single biggest risk that doesn’t get talked about enough. Over the past three decades, annual inflation has been about 3%, on average. It’s incredible that typical advisors don’t give inflation more attention to educate their clients’ giving that it has an approximate 20% negative impact on your retirement.

Catastrophic Illness or Death of a Spouse. We never know when life will occur. When a major illness, injury, or death occurs many people will have to dip into their retirement savings to make ends meet which makes it difficult to catch up if they ever do.

Life Solution Retirement & Life Protection for The Living

Life insurance is not just for a death benefit. There are many other benefits available that can grow and protect your retirement when life happens.

Tax-Free Retirement Account / Life Solution Living Benefits

Many of our top-rated carriers include living benefits at no additional cost. Living benefits allow you to use a portion or all of your policy death benefit If you experience a qualifying life event such as terminal, chronic, or critical illness, or critical injury.

There are no restrictions on what the benefit can be used for providing you and your family the flexibility to take care of what is important to you.

Examples of what the benefit can be used for:

Mortgage or rent payment

Home repair/modifications

Day to day bills

Daycare

Nursing home

Travel

In-home health care

Moving expenses

Terminal Illness

If you are diagnosed with terminal illness that will result in death within 24 months certifiied by a physician.

Chronic Illness

If you are not a able to perform two of the six ADL (activities of daily living) for a period of 90 consective days or you are cognitively impaired.

Activities of Daily Living

- Bathing

- Continence

- Dressing

- Eating

- Toileting

- Transferring

Critical Injury

- Coma

- Paralysis

- Severe Burns

- Traumatic Brain Injury

The information listed on this website is for informational purposes only. Each carrier and state have different guidelines on what riders are available and the percentage that can be accelerated. It’s important to discuss your policy with the carrier or a licensed agent for information that is specific to you and your state.